How To Use Payday Loans Without Getting Ripped Off

Payday loans are an easy way to get cash in a pinch. However, they can cause you to have a high balance on your account. To avoid this, you should look for alternatives to payday loans. Read this article to learn more about the alternatives. Once you find an alternative, you’ll know what to do to avoid getting ripped off by payday loans.

Alternatives to payday loans

If you’re in a pinch and need money fast but can’t afford a payday loan, there are a few alternative options. One of them is to get a cash advance on your credit card. Credit card advances have a lower interest rate and allow you more flexibility during repayment. You’ll still have to pay back the money you borrow, but it won’t cost you as much as a payday loan.

Another option is a stretch pay loan, which some credit unions have recently started offering. These loans are usually short-term and have low-interest rates, which makes them a good alternative to payday loans. These types of loans can be obtained through many different types of banks, credit unions, and online lenders.

Another alternative to payday loans is credit counseling. A certified credit counselor can help you manage your finances and make smart decisions. During the counseling session, you can discuss your debt and your priorities. The counselor will help you decide which bills are urgent and which are not. They will also introduce you to self-discovery tools to help you take charge of your finances.

Credit unions are another option. Credit unions often have lower interest rates than payday lenders, but the process can take days. These loans are not ideal for emergencies, but if you’re sure you’ll be able to make the repayments, a credit union loan may be the best option for you. Unlike payday loans, credit unions are often more flexible, and you can get a loan even if your credit score is low.

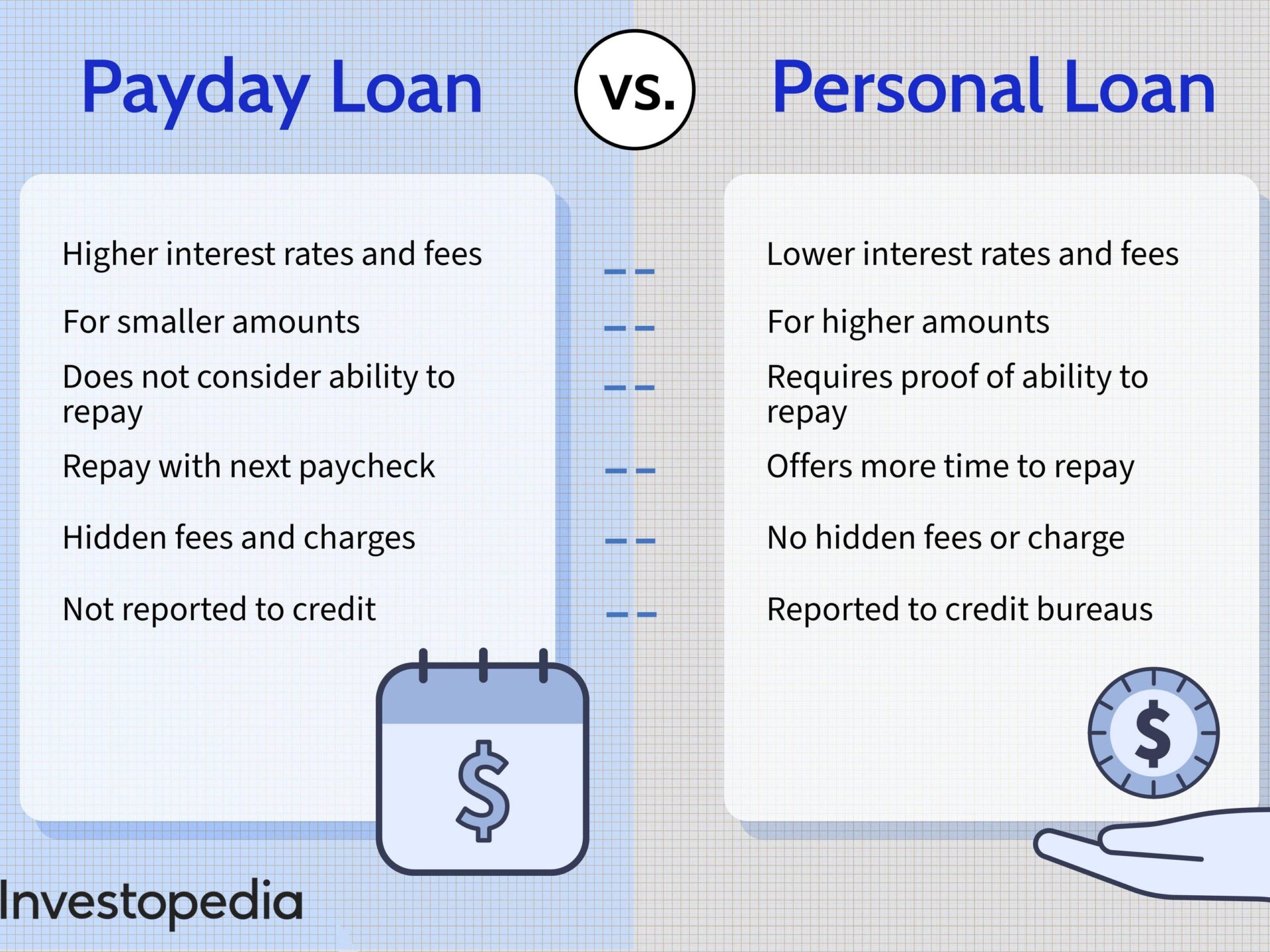

Another good option is a personal loan. This type of loan is generally secured by collateral. You can borrow up to $1,000 in an installment plan and pay it back with a smaller interest rate than a standard payday loan. A personal loan may be a great way to consolidate credit card debt. Pawnshops also offer personal loans, but they will usually have higher interest rates.

Besides credit unions, you can also try local lenders to get a small loan. Since they are owned by the people you bank with, they can be more lenient with their loan qualification standards. If you cannot find a local lender, credit card cash advances are also a good option. Although credit-card cash advances charge high-interest rates, they are generally lower than payday lenders.

Payday loans are helpful in emergencies, but they can be expensive and drain your money. These loans can also have a negative effect if you don’t pay them back on time. Another option is to take an auto title loan. This loan works much like a payday loan, but the lender uses your car title as collateral.

Payday loans are not difficult to get. Most of them don’t require a credit check and can be as little as a few hundred dollars. The repayment period is typically within a few weeks. The lender might connect to your bank account to take money on the due date, but it’s possible to extend the loan for a small fee.

Payday loans are generally a last resort for borrowers in financial emergencies. However, the high-interest rates and short payback periods make them hard to pay off. As a result, they should only be used when you need to raise money fast and don’t have any other options. However, you can find other, more reasonable alternatives that can help you make it to your next payday and build a financial cushion for the future.

Getting loans from family members and friends is another way to borrow money. Although you don’t need physical collateral, you should always keep in mind that these loans are meant to be temporary solutions. If you find yourself relying on them too often, you may need to evaluate your budget.

Another option for people in financial crisis is to use credit cards. A credit card can offer you an opportunity to borrow money without paying any interest and is a great way to avoid payday loan fees. However, these loans often come with high service fees and short repayment periods. A $100 loan with a fifteen percent service fee translates to a 391 percent annual percentage rate.

Another good option is a payday loan marketplace. These websites offer a variety of loans that are available online and can be approved within one business day. They are also popular with people in need of emergency funding. As an added benefit, many of these loans can be made through an easy, secure mobile application process. Depending on the company, you may be able to control the terms and conditions of the loan.

Another alternative to payday loans is peer-to-peer lending marketplaces. The process is similar to getting a personal loan from a bank or other financial institution, but it relies on your willingness to repay the loan. These sites will perform a credit check on you and assign you a rating based on how likely you are to pay it back. Other consumers may even be willing to fund the loan if they think you can pay it back. However, this option may not be right for people with bad credit.