Mortgage Tips To Save You Money

There are several ways to save money on your mortgage, and a number of these are described in this article. In this article, you’ll learn how to save money on your interest payments, calculate how much your mortgage will cost, and save money by paying your mortgage every two weeks. Among the many tips, saving money on your mortgage is a great way to pay off your loan sooner.

Saving for a down payment

When applying for a home mortgage, saving for a down payment is a big task. While most lenders like to see at least 20% down, this is not always possible in today’s housing market. Without a 20% down payment, borrowers will likely need to pay private mortgage insurance, which adds extra costs to the monthly payment. Here are a few tips for saving early. Keep a separate account for the down payment.

Down payment amount – The size of your downpayment will depend on your lifestyle and long-term financial goals. A larger down payment means lower monthly mortgage payments. It also means more money available to cover other costs, including property taxes, maintenance, insurance, and potential repairs. A larger down payment will also help you qualify for lenders’ lower loan-to-value ratio (LTV). You can also qualify for a more down interest eligible mortgage insurance with a larger down payment.

The best way to save for a down payment is to save money for several years. Saving up for a down payment can take a long time, but it can be worth it. A home mortgage consultant can show you all the available options and help you find the right one. In addition to saving money for the down payment, a mortgage consultant can help you compare the overall costs of the different options.

Another way to free up more money for savings is to get rid of debt. Paying off credit card debt, student loans, and car loans are your most significant expenses in saving for a down payment. As long as you can pay off these debts, you’ll be well to homeownership. The last thing you want is to spend all your available cash on a high monthly mortgage payment, not even a down payment.

Calculating interest payments on a mortgage

Mortgage payments are made to cover the loan balance and interest. They are generally consistent monthly payments. During the initial years of a mortgage, you make mostly interest payments. Then, as the loan term goes down, you will make fewer interest payments but still have to pay the loan balance. You can use a mortgage payment calculator to determine the best balance for your budget. Here are some tips for calculating interest payments on a mortgage to save you money

Using the amortization schedule on a mortgage is essential for determining how much your payment goes toward principal and interest. When you make extra payments on your mortgage, more of it will pay down the principal. Paying down the principal balance sooner saves you money. When calculating your mortgage payments, it is best to pay extra money to the principal balance rather than interest. Using the amortization schedule can save you a significant amount of interest.

The monthly payment on a $200,000 fixed-rate mortgage will take 360 months to pay off. With an annual interest rate of 4.5%, that’s $1,013. However, the figure does not include real-estate taxes, homeowners insurance, and private mortgage insurance. The monthly payment on a $200,000 mortgage with a 4.5% interest rate equals 0.375% of the loan balance.

Once you know your monthly payment amount, you can make it more affordable by choosing a biweekly mortgage payment. This way, you’ll be making two extra payments in a year. This will allow you to pay down your mortgage faster, saving you thousands of dollars in interest. For example, if you pay a $5,000 mortgage in 12 months, you’ll only have to pay $25 every month for good.

Paying your mortgage every two weeks can save you money.

Biweekly mortgage payments can make your payment schedule more manageable and save you money in the long run. You will only have to make payments every two weeks for two months out of the year instead of six. This is advantageous because you’ll build up more equity in your home, which you can then borrow against for various purposes. However, paying your mortgage biweekly may not be the best option for everyone. It can stretch your budget.

Biweekly mortgage payments can save you money in many ways. First of all, they reduce your overall debt. You can save thousands of dollars in interest alone by paying your mortgage every two weeks. Secondly, you’ll pay off your loan sooner. By paying your mortgage every two weeks, you’ll pay off your loan in just over half the time. Biweekly mortgage payments can also reduce the number of years you’ll pay off your loan, as most mortgage terms are between 15 and 30 years.

Another way to save money on your mortgage is to split it into two equal payments. The difference is that biweekly payments equal thirteen monthly payments instead of four. For a year, that’s 26 biweekly payments. This means that the extra payment you’ll make annually won’t affect your monthly payments as much. Moreover, biweekly payments can help you save money because you’ll have the extra income to make other purchases.

However, biweekly mortgage payments may not be suitable for everyone. It’s important to consider how biweekly payments fit your budget, payment schedule, and lender’s fees. Regardless, you can save money on your mortgage by making an extra $50 payment every two weeks. This extra money can pay for other expenses, such as vacations, entertainment, or a new car.

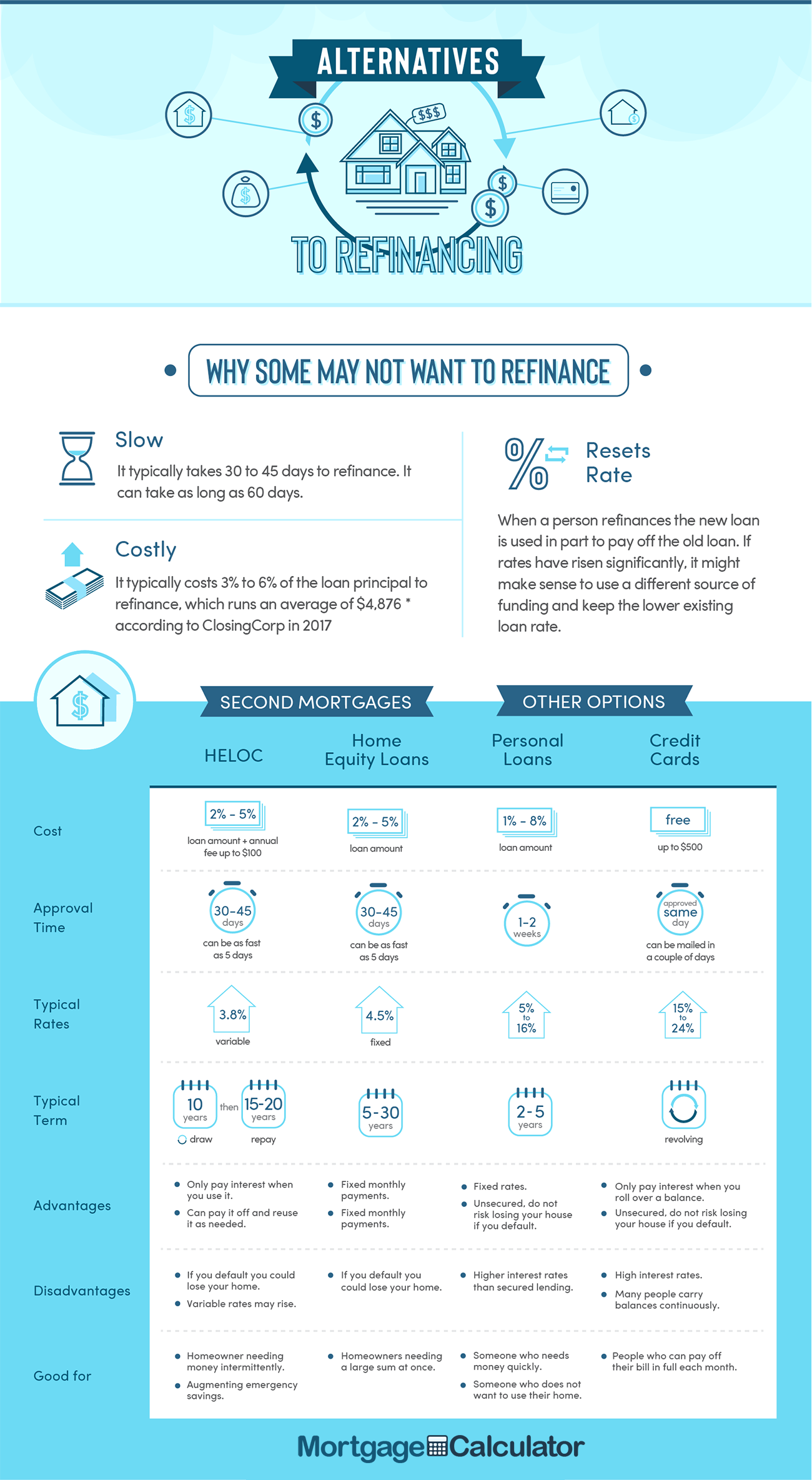

Saving for a HELOC or fixed-rate second mortgage

If you want to take out a HELOC to pay off your debts, there are some essential things you should know before you begin. The interest rate is one of the most significant factors that you should keep in mind, as you will have to pay back the loan with interest, and your home is collateral. While this may not sound like a big deal, it can put you in an uncomfortable situation. Another issue is interest rate risk, as most HELOCs are variable, which means that if the interest rate goes up, your repayments will increase.

A HELOC has two phases: the draw period, during which you can tap into the credit line, and the repayment period, after which you must repay the loan with the principal plus interest. You can also make principal payments during the draw period, which will make the transition to the repayment period a bit easier. However, you will need to make sure that you can afford the payments on your second mortgage. Otherwise, you may end up with a balloon payment.

If you consider a HELOC as a financial safety net, you should know that it may be challenging to obtain one. Many large banks stopped issuing them in 2020 due to the economy. Many of them haven’t yet returned. Retirees have the most challenging time qualifying for a loan. However, if you have sufficient savings, a HELOC is a great way to supplement your income, especially when the stock market is down.

Another factor to consider is the monthly payment. Because of the lower interest rate, a second mortgage is usually more accessible to budget. However, an ongoing line of credit may be more challenging to manage. Because your monthly payments will be primarily based on interest and withdrawals, make sure you can comfortably handle the extra cost. You should also factor the additional loan payment into your monthly budget. However, make sure you can make the payments on time to avoid foreclosure.

Shopping for a lower interest rate

Some tips can help you get a lower interest rate on your home mortgage. First, remember that mortgage rates aren’t always apples-to-apples. Rates advertised by lenders are based on a best-case scenario, which assumes a 760 credit score, 20% down payment, and a single-family home. The reality is that your mortgage rate will likely be higher.

The longer your home loan term, the more money you will need to save for your down payment. Putting more down on your home is an excellent way to increase your equity. However, it would help if you considered that the interest rate is tied to the length of your loan. A 15-year fixed-rate mortgage will typically have a lower interest rate. Lastly, if you have a good credit score, you can opt to pay extra points to get a lower rate.

Although advertised rates can be tempting, please don’t fall for them. These rates often come with fees and discount points that will make your APR higher than you qualify for. It is always wise to shop for the lowest interest rate, even if it means sacrificing a bit of peace of mind in the short run. For example, a 30-year fixed-rate mortgage currently stands at 3.78%. You can lock in that rate for as little as 0.8 points and fees.

While shopping for a lower interest rate on a home mortgage is a great way to save money, it’s important to remember that mortgage rates are rising, so it’s essential to lock in your rate as soon as possible. Likewise, if you’re buying a house in a competitive market, you may have to compete with a potential buyer for the property. You can secure a lower interest rate if you’re organized by planning.