10 Tips For Buying Life Insurance

When looking for life insurance, you have several choices. You can purchase term life insurance, whole life, universal life, or a burial policy. However, you need to make sure you get a full picture of your financial health and then decide what type of coverage you need. Here are 10 tips to consider before purchasing life insurance.

When looking for life insurance, you have several choices. You can purchase term life insurance, whole life, universal life, or a burial policy. However, you need to make sure you get a full picture of your financial health and then decide what type of coverage you need. Here are 10 tips to consider before purchasing life insurance.

Term life

Term life insurance is a type of life insurance that covers you for a specified period. During the term, the policy pays out a death benefit if you die. However, if you live past the term, your beneficiaries will not receive anything. However, most term life policies will guarantee the same insurance premiums and death benefit amount.

Term life insurance is also commonly offered by employers as a benefit to employees. It provides financial protection for those who cannot afford a permanent life insurance policy. It also provides coverage for dependent children of the policyholder. The death of a loved one is a heartbreaking experience that can affect every area of a person’s life. This is why planning ahead is important.

Term life insurance is a popular choice for people with young families. Although the premiums are relatively inexpensive, it is important to understand that this type of policy will only cover you for a specified period. For younger families, term life insurance is a better choice because it allows them to select how long they want to remain insured. Moreover, death benefits from a term life insurance policy will not count as taxable income.

Whole life

Whole life insurance, or whole life assurance, is a policy in which you build cash value over your entire lifetime. This cash value is actuarially designed to equal your death benefit. The policy is permanent and cannot be changed or canceled. This makes it one of the most secure investments. If you die before your policy matures, you can access your cash value as cash when needed.

The downside of whole life insurance is that it is more expensive than term life insurance. However, the cash value of the policy will continue to grow over time, giving you the ability to use it to meet unexpected expenses. This cash value can be used to upgrade your home or expand your business or provide income during retirement.

Whole life insurance can have a few different types. One type offers level premiums for the life of the policy. You can use these payments to pay off debts or leave a legacy. Another type of whole life insurance will let you borrow against the cash value of the policy if you need it.

Universal life

Universal life insurance is a type of permanent insurance that is designed to last for life. However, the policy may have higher premiums than a traditional whole life insurance policy. Those who decide to opt for this type of insurance should consider their personal financial goals and whether they can pay higher premiums in the beginning. They should also consider their estate planning needs before purchasing permanent life insurance.

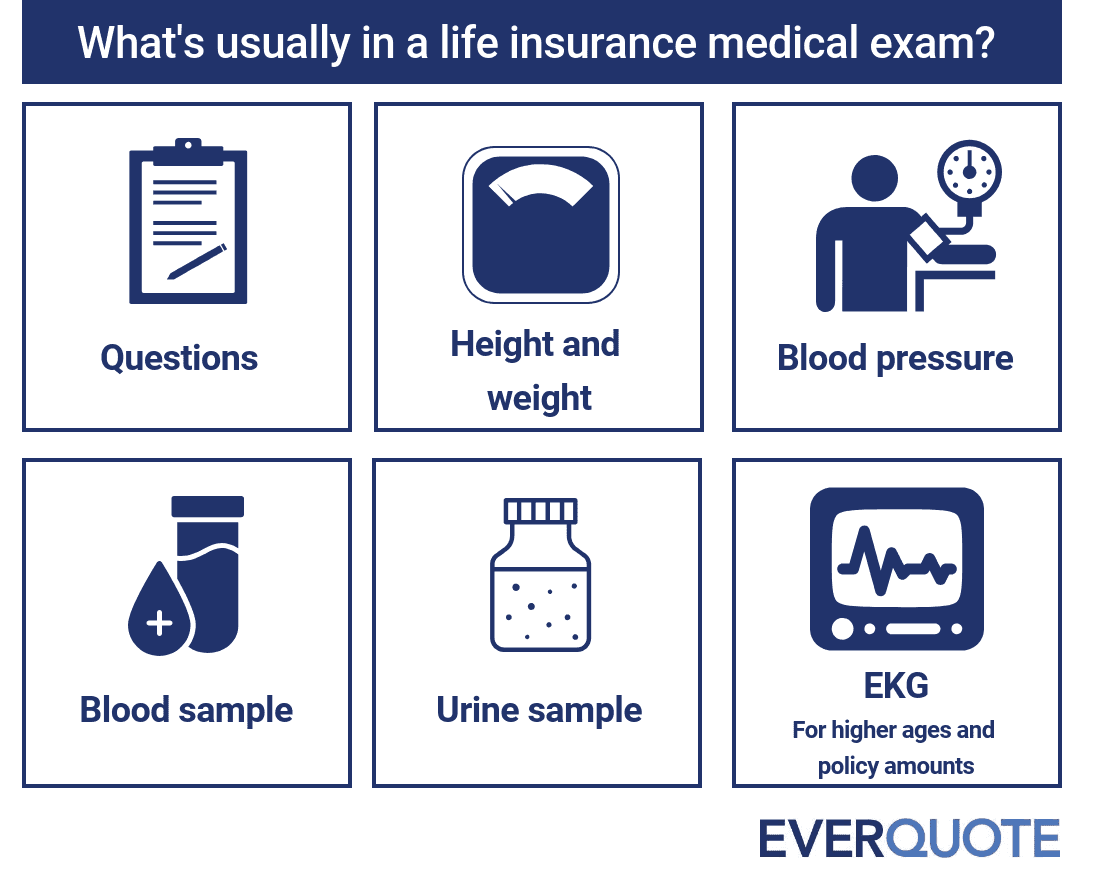

Applicants for this type of life insurance must complete an application and provide some basic personal information. The insurance company will also conduct a health exam and determine the premium amount. Once this is complete, they must sign the required documents, pay the first month’s premium and designate a beneficiary. They may also choose to add riders to their policy, which provides additional protection and flexibility.

There are many advantages to universal life insurance. The policy’s cash value grows over time and is accessible to beneficiaries in the event of the policyholder’s death. Some universal policies also allow policyholders to take out a loan from their cash value, which can increase their death benefit. This type of policy also allows policyholders to adjust the death benefit as needed.

Burial policy

Burial insurance is a way to protect loved ones from the costs of their final arrangements after a loved one passes away. This policy can be purchased from most life insurance companies or through funeral homes in some states. Purchasing a burial policy is simple: simply submit a surrender form and receive a check for the cash value of the policy. This money will then go to the beneficiary of the deceased’s policy.

Burial life insurance is available to anyone who qualifies for the policy. Typically, a policy will have a graded death benefit which is equal to the number of premiums paid and interest on the policy, up to a certain limit. However, accidental deaths are usually covered in full. Another benefit of a burial policy is that it is a guaranteed-issue policy. This means that any person can apply without having to undergo a medical exam or answer health questions.

The cost of a burial policy is relatively low compared to other types of life insurance. The average monthly premium for a burial insurance policy is around $100. However, the policy will have different terms depending on the company. Some will accumulate cash over time, while others will allow the borrower to borrow against the value. However, if the policy pays out quickly, this will ensure that the family has the funds to cover any final expenses.

Final expense policy

A final expense policy is something to consider when you’re looking for life insurance. These policies can protect your beneficiaries from having to use the proceeds from your general life insurance policy for the funeral expenses of your family. While they’re more expensive, they can be a good choice if you’re unable to find affordable term life insurance with a waiting period.

Another advantage to final expense insurance is its ability to ease the financial burden on your loved ones after your death. While estate settlement can take months, you don’t want your loved ones to be left in a financial crisis. With final expense insurance, your loved ones can receive the money they need immediately. In addition to being affordable, these policies build up cash value over time, which can be used as collateral during your life. In addition, the death benefit can’t be reduced if you have a medical condition.

A final expense policy can be beneficial for those who want their loved one’s funeral expenses covered immediately. However, there are many factors to consider when purchasing such a policy. For example, some policies only cover funeral expenses, while others only cover certain debts. The best way to determine which type of policy is the best one for your family is to compare the costs and benefits of different plans.

Affordable options

Life insurance can provide financial security for your loved ones after you die. It can cover funeral expenses, pay off your mortgage, and replace your income. However, finding affordable life insurance for people with pre-existing medical conditions or high-risk occupations can be a challenge. These people should consider hiring an impaired risk specialist to find a policy that fits their specific needs. Other affordable options include no-exam life insurance.

Considerations before buying life insurance

Life insurance is an important part of any financial plan and should be carefully considered. Not only does it provide a financial safety net for your loved ones, but it can also help pay off your mortgage or put your children through college. While money will never replace the loss of a loved one, it can make it easier for your family to live the life you planned.

To get a life insurance policy, you must complete an application, which will include your personal and family medical history. You may also have to undergo a medical exam. You will also need to disclose preexisting medical conditions and a history of accidents and DUIs. Additionally, you will be asked to provide standard forms of identification.

You should analyze your financial situation to determine how much money is necessary to cover funeral expenses. You should also figure out how much money your beneficiaries will need to live comfortably. Then, you should compare the various types of policies available, as well as their premiums. After all, you need to make sure that you can afford the premium.